Saving for the Apocalypse

How I Learned to Create an Emergency Fund

In Karen McCall’s book Financial Recovery: Developing a Healthy Relationship with Money, she argues that you must save your way out of debt. If you don’t, even if you manage to claw your way out, you’ll perpetuate the same cycle of debting. You must learn a replacement habit, and the replacement habit is not Paying Off the Debt Once or Not Overspending for a Little While. The replacement habit is Saving.

For me, money has always been a juggling act. I came of age when rent was reasonable, student loans were a given, and credit card interest rates were low. As a college student, I was financially independent but never had savings. Instead, I waited tables in busy restaurants where I left each shift with a wad of cash. When I needed—or wanted—something extra, I used a credit card. I paid my bills on time. I had an excellent score.

I assumed I’d be in debt forever.

After my husband and I bought a house, credit card debt was rolled into a HELOC, with a lower interest rate and tax-deductible interest. I thought about money all the time, the way a heartsick girl misses her boyfriend, in a kind of anxious attachment. As soon as a paycheck arrived in our joint checking account, I flung it in every direction. I paid bills immediately. I stocked up on groceries. I ordered the kids new clothes. It wasn’t unusual to be “broke” three days after payday. I still had an excellent credit score. And I was still juggling debt, dipping into and repaying our home equity line of credit every other week.

Sometime around 2019, my husband came home for lunch, walked into the living room a little too quickly, and handed me a yellow Post-It note. It was the raise he’d been promised, a promotion that his boss had been championing for months. The raise was significant, in the five figures. $10,000? $20,000? I don’t remember the number. I do remember his softened face, a little boyish, a brief respite from his Resting Pessimism Face.

And I remember a sick, Oh, Shit, feeling that ran through my body, landing heavily in my gut. This is it, I thought, the room spinning a little. No more excuses. Now we have to get our shit together.

More money in our family budget was a gift, an opportunity. But savings, it turns out, is tricky. What counted as savings? How long do you have to hang for it to count? What happens if you intentionally save for something and then spend the money? How can you be sure you really saved at all?

Financial Recovery divides savings into three categories: Deferred Spending, Emergency Savings, and Long-term Investments. In fairness, we *were* saving money, some money. But it turns out that being a grown-up means saving money in lots of different places.

Long-Term Investments

We were putting away money for our kids’ college, in 429 accounts. I had started one for our first son, in the months after he was born. I guffawed when the calculator instructed me to save $500/month, every month of his life, in order to afford college in eighteen years. I was sure the calculator was lying. (I mean, we are Midwesterners. Our kids are not Ivy League bound.) I was also sure that I was already failing. I began anyway, with $25/month, and that number grew as our budget allowed.

We had retirement accounts, and jobs that provided some sense of secure retirement, whatever that means in this day and age. I actually had two accounts, and between them I was saving nearly 20% of my paltry but stable salary. Jim’s retirement was tied in with a variable profit-sharing scheme that landed in the 9-13% range most years. We weren’t heading towards FIRE, but we were making respectable progress towards not eating dog food in retirement.

We had some equity built up in our house, which we were on pace to pay off in 15 years. The house that you live in may or may actually be an investment, but if nothing else, it created a sense of security.

Deferred Spending

The first time we had something resembling the savings of “deferred spending” was a year after Jim’s raise, and this, too, came from a windfall. #ThanksBiden. The American Rescue Plan money went into savings, for a few months anyway. We couldn’t travel, we were well stocked on sweatpants, and given all the time we were spending at home, the house projects were starring us down. So we built up a little savings, but soon we spent it on a dog ($800) and a fence ($2300) and some plumbing ($1100). So we saved a little more and felt good about ourselves, like we were proper grown-ups. And then our boiler died ($4000).

It had felt so good to have that money waiting for an “emergency” and it was so very painful to spend it. In my favorite social media group, Women’s Personal Finance, I’ve seen women ask if they should use a credit card for a surprise car repair when they have $25,000 in liquid savings. Nothing about that makes sense, but it speaks to the feeling of safety that money provides.

Emergency Savings

As I’ve learned to save, as I’ve created more honest budgets that don’t hide from myself where we’re actually spending money, I found the idea of an “emergency fund” grated me. I mean, if you create enough categories for occasional expenses, if you plan for house projects, if you have excellent health insurance that won’t leave you bankrupt should you have a baby (me + me) or need major surgery (me + me), if you have double dental insurance (me), if you have two working partners who each have secure jobs and life insurance and long and short term unemployment insurance, what is an emergency fund for? And how does anyone actually save 3-6 months worth of living expenses?

Two years ago, I set the question to Women’s Personal Finance (Women On FIRE), the wise and generous Facebook group I had learned so much from. I explained that my priorities were

Paying off our mortgage in 9 years (We were paying ~$250/extra each month so it could be cleared a few years before Jim retired)

Playing catch up on retirement (I was still saving 20% while Jim was up to 15%)

Paying into 429s for our kids

And I asked the question: “Am I deluding myself by not putting more money into a HYSA for emergencies and instead using our HELOC, should the need arise?”

When I read that question today, I can see that I was really saying: “Isn’t this enough? Aren’t I doing such a good job? Do I really have to do all the savings things?”

The truth was, I still didn’t understand what kind of emergency I might ever need that money for. I still had good credit, and too many credit cards, though just one with a balance, a 0% card taken out to finance our air conditioning installation.

The wise women of the internet did not disappoint. Within a couple of hours, there were 56 comments.

One poster pointed out that maybe I didn’t as much control over our budget as I thought I did.

How do you plan to buy the next car? Do you have to wait until your A/C is paid off and then you’ll find financing for the car? Sounds like you do need to start setting money aside for upcoming purchases let alone emergencies. I’m typically ok with a small emergency fund, I don’t make it my top priority, but I still think something needs to be available to have true financial stability.

A few others pointed out how much more control I’d actually have if I didn’t just hand extra money over to the bank every month.

Even without the discussion of the emergency fund, If you want to pay off your mortgage faster it actually makes more sense to put that $250/month into a HYSA earning 5% interest than to your 2.5% mortgage. When the amount in your HYSA equals your balance due on the mortgage, you can pay off the mortgage in one lump sum. Paying off your mortgage will actually happen sooner this way because the money is earning interest this whole time (and added bonus if u have a true emergency like a job loss the money is easily accessible).

After this outpouring of advice, I realized two things:

It (still) turns out that being a grown-up means saving money in lots of different places.

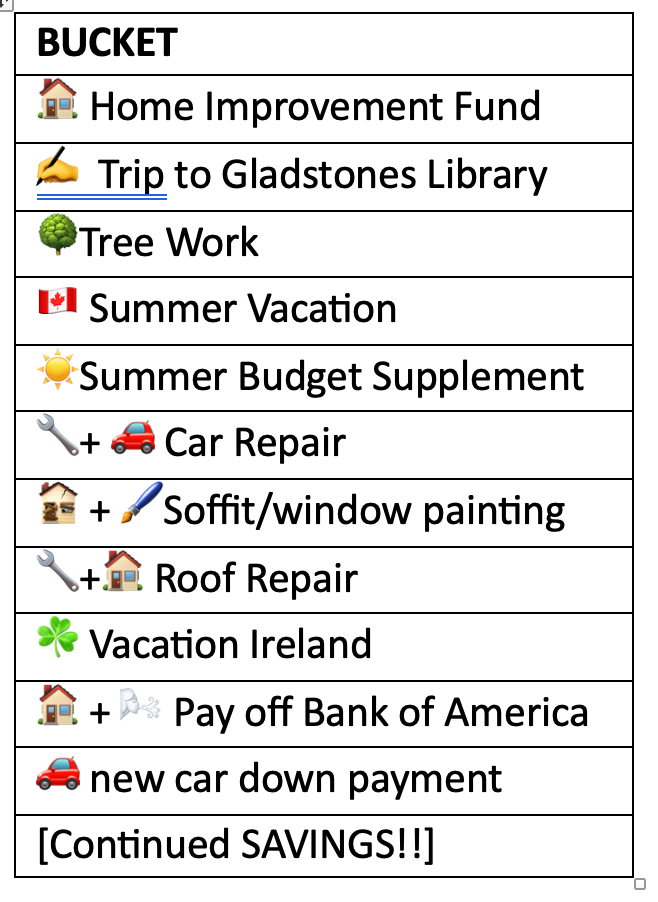

I had set up two “deferred spending” savings accounts, one for home and car expenses, and a second for vacation and summer money, but that was no longer enough buckets. I had an emoji-filled spreadsheet tracking progress on a series of goals so that I wasn’t fudging the numbers, but my actual plans for any of the items had blurred. I needed more savings accounts.

I now had the discipline to not hand over extra money to the bank every month.

I could cut back on the Long-Term Investment category in service of liquid savings, taking the $250/month I was overpaying on the mortgage and giving it two jobs.

I could create an “emergency savings” account for the apocalypse—we had to flee the country in political upheaval, or the house needs major structural repair, or the bank closes our HELOC or raises the interest rate to an uncomfortable level. I could let that $250 accumulate every month, and let it earn interest, and let it provide me and my family with security.

And if and when I wanted to, I could still use it to pay off the mortgage early.

Were any of those emergency scenarios likely? God, I hoped not, but that was the definition of an emergency. Maybe I had to imagine one to give myself a reason to fund it. And I knew that last reason, about rising interest rates, was not such a distant, unrealistic fear. It was already happening.

I had come of age on cheap credit, and so I believed credit would always be freely and cheaply available. Emergency savings was for a world where that was no longer the case.

Questions for Writing & Reflection

How did you learn to save money? If you are starting now, what is a small goal you can work toward?

What does an emergency fund mean to you? If you’ve saved the 3-6 months of funds recommended by experts, how did you do it?

What does your dream of financial security look like?

I think there's this cultural idea that if you own your house, that's financial security. It turns out, it's more complicated than that.

I very much enjoyed this one. Most of my adult life has been spent gaining financial literacy.